What is Reverse Charge Mechanism in GST (Goods & Service Tax)

Summary: Understanding the complexities of RCM in Goods and Services Tax (GST) is crucial for businesses to ensure compliance and operational efficiency within the tax framework. Analyzing RCM implications and utilizing self-invoicing tools can help streamline financial processes and enhance transparency in tax management. Let’s learn more about it.

In the realm of Goods and Service Tax (GST), understanding the depth of Reverse Charge Mechanism is crucial for businesses and taxpayers. This mechanism has been designed to shift the responsibility of tax payments from suppliers to the recipients, representing a significant shift in tax compliance.

This shift not only impacts the time of supply but also mandates record-keeping and compliance to ensure seamless tax governance. Therefore, understanding RCM GST is crucial for businesses to navigate the complexities of GST regulations and maintain compliance with provisions outlined in the Act and Rules.

In this article, we will understand different aspects of reverse charge mechanism, for both goods and services while reshaping tax obligations for businesses.

What is Reverse Charge Mechanism (RCM)

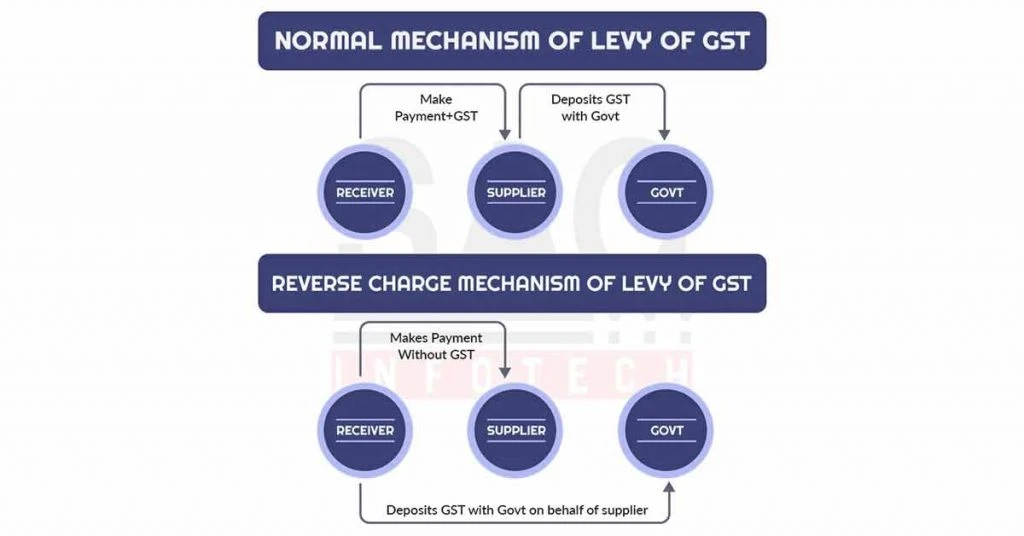

RCM on GST refers to the process in the GST system within India, where the recipient of any product/service is required to pay GST rather than the supplier. In simple terms, the responsibility to pay tax for goods/services shifts from the seller to the customer.

Some important key pointers regarding RCM include:

- It only applies to certain supplies identified by the GOI, including imports of goods/services, and purchases made from any unregistered dealers.

- The recipient should be registered as a GST taxpayer.

- Recipients need to make GST payments to the government later, they can claim an ITC (input tax credit) for the tax paid.

What is Normal GST Mechanism?

The standard GST process is a straightforward procedure as compared to the RCM process. Here’s a breakdown of how it functions:

- Supplier’s GST Charging: When a registered supplier sells goods/services to a customer, whether registered or unregistered, they include the GST amount in the invoice. Here, the GST rate is determined based on the specific type of goods/services supplied.

- Customer Payment Inclusion: The customer pays the supplier the total invoice amount, which consists of the GST component.

- GST Deposit by Supplier: The registered supplier accumulates the GST amount from all their customers throughout a tax period. Later, they deposit the collected GST funds to the government.

- Input Tax Credit (ITC): The supplier has the provision to claim ITC for the GST paid on their business-related purchases like raw materials, office supplies, etc. This ITC serves as a deduction against the GST payable on their sales, thus preventing double taxation.

When is the Reverse Charge Mechanism Applicable Under GST?

The Reverse Charge Mechanism in GST under the Goods and Services Tax (GST) is applicable in specific scenarios, typically involving transactions with unregistered dealers, designated goods, and services as outlined by GST law, and imports of services or goods.

Businesses should carefully assess their transactions to identify cases where RCM is applicable and adjust their financial and compliance frameworks accordingly. This approach is important in ensuring complete adherence to RCM provisions, mitigating risks, and maintaining robust tax compliance according to GST regulations.

Input Tax Credit (ITC) in RCM

Input Tax Credit (ITC) in the context of Reverse Charge Mechanism in GST holds an important role in the implications for businesses under the Goods and Services Tax (GST) framework. When a recipient pays tax under RCM for goods/services received, they are eligible to claim ITC for the tax paid.

This mechanism allows businesses to deduct the tax liability against the tax they are required to pay on their outward supplies. This thereby prevents double taxation and fosters a more seamless tax structure.

Understanding the concept of ITC in the RCM framework is important for businesses to optimize the process of tax management, enhance financial transparency, and ensure compliance.

Time of Supply Under RCM

The time of supply refers to the moment when the supply becomes liable to GST. One of the crucial factors for analyzing the time of supply is when the entity is responsible for paying the tax. In the particular case of reverse charge, the recipient holds the liability to pay GST.

Therefore, the time of supply for goods and services under reverse charge differs from those under normal charge.

For the supply of goods, the time of supply is the earliest of the following:

- The date of receipt of goods.

- The payment date as per the account books or the debit date in the bank account, whichever occurs first.

- The date immediately following thirty days from the date of issue of the invoice or a similar document.

In the case of the service supply, the time of supply is the earliest of the:

- The payment date mentioned in the account books, or the debit date mentioned in the bank, whatever is earlier.

- The date immediately following sixty days from the date of issue of the invoice or a similar document.

Registration Rules in RCM

In the context of GST, registration rules under the Reverse Charge Mechanism are of utmost importance for businesses. Under RCM, businesses liable to pay tax on procurements are required to register under GST, having a threshold limit of INR 20 Lacs (note: INR 10 Lacs for special states, excluding J&K).

Additionally, businesses dealing with RCM are obligated to file their tax returns and adhere to compliance requirements. Understanding and proactively engaging with registration rules in RCM is essential for businesses to ensure compliance.

Who Should Pay GST Under RCM?

Determining who should pay the Goods and Services Tax (GST) under the Reverse Charge Mechanism (RCM) is important for businesses to have better clarity regarding taxes and deductions.

Under RCM, the liability to pay GST shifts from the supplier to the recipient in specific scenarios like:

- Transactions with unregistered dealers

- Designated goods/services

- Imports of products/services

Businesses need to identify these cases without any miss to fulfill their tax obligations promptly and maintain records to ensure compliance and avoid penalties.

Supplies of Goods Under Reverse Charge Mechanism (RCM Goods)

Here’s the GST RCM list of goods that are subject to the Reverse Charge Mechanism in GST. These include:

| List of Goods | Recipients of Goods |

| Cashew Nuts, Bidi Wrapper Leaves, Tobacco Leaves | Supplied by an Agriculturist to any registered person. |

| Lottery | Supplied by the State Government, Union Territory, or any local authority to a lottery distributor or selling agent. |

| Silk Yarn | Supplied by any person manufacturing silk yarn from raw silk or silkworm cocoons for the supply of silk yarn to any registered person. |

List of Supplies Service Under Reverse Charge Mechanism (RCM Services)

Here’s the list of services that are subject to the RCM. These include:

| List of Supplies | Recipients of Supplies |

| GTA Services | Provided by a Goods Transport Agency to any entity. |

| Legal Services by Advocate | Rendered by an individual advocate or a firm of advocates to any business entity within taxable territory. |

| Services by an Arbitral Tribunal | Supplied to a business entity. |

| Sponsorship Services | Extended to anybody like a partnership firm or corporation. |

| Government Provided Services | Excluding specific categories, provided by the State and Central Government, Union Territory, and local authority to a business. |

| Services Provided by a Director | Offered by a director of a company or a body corporate to the said company or body corporate. |

| Services by Insurance Agent | Provided to any person carrying out the insurance-related business within the country. |

| Services by a Recovery Agent | Supplied to a banking company, a financial institution, or a non-banking financial company. |

| Copyright Services | Provided by an artist, music composer, author, photographer, or the like to a publisher, music company, producer, or similar entities. |

These provisions shed light on compliance requirements of the reverse charge mechanism under GST (especially, the CGST/WBGST Act, 2017).

Liability of Registration Under RCM (Reverse Charge Mechanism)

Under the Reverse Charge Mechanism (RCM), the liability for registration is a key consideration for businesses. Any business that falls under the RCM is required to register under the Goods and Services Tax (GST).

This crucial requirement requires businesses to proactively engage with the registration process, comply with the regulatory framework, and fulfill their tax obligations to ensure seamless operations and adherence to GST regulations.

Important Points to Consider Under Reverse Charge Mechanism

Navigating the Reverse Charge Mechanism (RCM) in the domain of GST demands careful attention to several crucial considerations.

- It’s important for businesses to accurately identify instances where RCM is applicable, maintain records, and proactively manage their tax obligations.

- Understanding the implications of Input Tax Credit (ITC) under RCM, assessing the timing of supply, and ensuring compliance with registration and tax payment requirements are crucial components.

- Businesses should understand the difference between supplies of goods and services under RCM and remain well-informed regarding specific rules and regulations governing each category.

- Additionally, tracking and managing the liabilities associated with RCM, including accurate reporting and documentation, is important to cut off potential risks and maintain regulatory adherence.

By following these important points, businesses can promote tax compliance, and smoothen their financial processes within the GST framework.

Role of Self Invoicing

Self-invoicing can significantly streamline the procurement process for businesses, enabling them to create and issue invoices to themselves for purchases and related expenses. This approach boosts greater control, transparency, and compliance within the financial framework.

Several tools are available to help businesses in implementing self-invoicing seamlessly. Some of the popular solutions include QuickBooks, FreshBooks, and Zoho Invoice, each offering user-friendly interfaces, robust features for invoice generation, and automation capabilities.

Other options, including Wave and Xero, which provide a comprehensive platform to facilitate the efficient creation and management of self-invoices. Implementing these tools can enhance accuracy, expedite invoice processing, and empower businesses to navigate the complexities of self-invoicing within their financial operations.

Conclusion

Understanding the complexities of RCM in the Goods and Services Tax framework is crucial for businesses to navigate the tax landscape and ensure compliance. By analyzing the implications of RCM on cash flows, timing of supply, input tax credit, and registration requirements, businesses can meet regulatory obligations.

Moreover, introducing self-invoicing tools facilitates streamlined invoicing processes, and enhances transparency, control, and compliance within financial operations.

Ultimately, by integrating these insights and tools into their operational framework, businesses can foster a more efficient, compliant, and transparent financial environment within the GST framework.

Reverse Charge Mechanism in GST Related FAQs

What is the reverse charge mechanism in GST with example?

The Reverse Charge Mechanism or RCM in GST shifts the tax liability from the supplier to the recipient. An example is when a registered business procures services from an unregistered vendor. This makes the recipient liable to pay the GST rather than the supplier.

On which items RCM is applicable?

RCM applies to specific conditions including transactions with unregistered dealers, designated goods/services outlined by GST law, and import of services/goods.

What is the reverse charge method?

The reverse charge method is a mechanism in the GST system where the liability to pay tax shifts from the supplier to the recipient in specific scenarios outlined by GST regulations. It is designed to ensure the effective collection of taxes.

What happens if RCM is not paid?

If the RCM is not paid as and when required, it can result in non-compliance with GST regulations. This will lead to penalties, interest charges, and some legal requirements. It is hence important for businesses to meet RCM obligations to adhere to regulatory compliance.

Written by

Namrata Samal ![]()

Namrata is a skilled content writer with an expertise in writing marketing, tech, business-related topics, and more. She has been writing since 2021 and has written several write-ups. With her journey with Techjockey, she has worked on different genres of content like product descriptions, tech articles, alternate pages,... Read more